NewGeography.com blogs

The doubtful claim that low density US cities impose a cost to the economy of $400 billion is countered by their being the most affluent in the world. Nine of the top 10 cities in GDP per capita are in the US and more than 70% of the top 50. The highest GDP per capita city in the world is one of the least compact, Hartford, with an urban population density among the bottom 10 out of more the than 900 urban areas larger than 500,000 (See here and here).

Mobility is an important driver of economic performance. US cities have less traffic congestion, and shorter work trip travel times than their international peers (Los Angeles has the shortest work trip travel times of any megacity for which there is data). The key to this productivity is more dispersed residential and employment locations (less than 10% of jobs are downtown) and the less intense traffic congestion that is associated with such development. In the US, just as in Western Europe, commuting by car is much faster than by transit. The coming fuel efficiency improvements will narrow or eliminate the gap between personal vehicle and transit GHG emissions per passenger kilometer. US fuel efficiency standards are projected to reduce gross car GHG emissions by more than a quarter by 2040, according to the US Department of Energy. That's before any de-carbonization.

The US has some of the best housing affordability in the world (excluding cities like San Francisco and Portland, where politically correct policies raise prices, lowering the standard of living and increasing poverty). The miniscule reductions from favored urban policies are exceedingly expensive per tonne and incapable of making a serious contribution to GHG emission reduction.

Maintaining the standard of living and reducing poverty requires cities that are mobile and affordable. It is important that GHG emissions reductions be chosen for their cost effectiveness, rather than consistency with expensive academic theories that long predate GHG emissions reduction concerns.

This piece was posted to comments at The Economist.

by Anonymous 08/13/2014

What’s often forgotten in politics and governance is municipalities are the creation of state legislatures. A good deal of the population growth in major cities in the second half of the nineteenth century was due to annexation. One of the best examples is New York‘s amazing growth due to annexing Brooklyn. Few people are talking about it but it’s time to consider smaller political units. As Detroit struggles with failure of bankruptcy, the geographical size of the Motor city is becoming a major issue.

Detroit’s long decline eventually put it a federal bankruptcy court. The reasons are numerous but the reality is here. How Detroit exists from bankruptcy court is now an issue. Putting Detroit on a sound economic footing is essential to preventing another bankruptcy. The Detroit Free Press reports:

The investment banker representing the City of Detroit had talks with billionaire real estate investor Sam Zell and investment firm the Blackstone Group about selling them the city’s vacant property — but the investors weren’t interested, the Free Press has learned.

The revelation comes as the value of Detroit’s abandoned and blighted property — which the city considers assets in its Chapter 9 bankruptcy — is in dispute.

Creditors argue that city-owned property is a source of significant value that is being ignored in the city’s bankruptcy restructuring blueprint, called a “plan of adjustment.” The creditors argue the approximately 22 square miles of vacant or blighted property the city owns could be sold — with the proceeds distributed to creditors and even reinvested in the city.

But Ken Buckfire, president of the city’s investment banking adviser Miller Buckfire, testified that city-owned land “to some extent has negative value,” according to a deposition transcript obtained by the Free Press.

One way to interpret the comment about “negative value” is where the land is located. If Michigan’s state legislature re-drew Detroit‘s geographical boundaries, investors would be more interested in the land. A new municipality, without Detroit’s corrupt and expensive politics would be a major reform. Detroit as it exists today isn’t viable for job growth and a stable population. Detroit’s local politicians and special interest groups would obviously fight any changes in geographical boundaries in Michigan’s state legislature because a declining Detroit was a way to plunder taxpayers. But Michigan taxpayers need to start asking themselves: is Detroit’s 143 square miles a viable long term enterprise?

Maps have been published illustrating the City Sector Model functional urban classifications for the 52 major metropolitan areas in the United States. The maps are available at Demographia City Sector Model Metropolitan Area Maps.

Functional Classifications of Metropolitan Areas

The City Sector Model allows a more representative functional analysis of urban core, suburban and exurban areas, by the use of smaller areas, rather than municipal boundaries.

The nearly 9,000 zip code tabulation areas of major metropolitan areas are categorized by functional characteristics, including urban form, density and travel behavior. There are four functional classifications, the urban core, earlier suburban areas, later suburban areas and exurban areas. The urban cores have higher densities, older housing and substantially greater reliance on transit, similar to the urban cores that preceded the great automobile oriented suburbanization that followed World War II. Exurban areas are beyond the built up urban areas. The suburban areas constitute the balance of the major metropolitan areas. Earlier suburbs include areas with a median house construction date before 1980. Later suburban areas have later median house construction dates.

A New York Times article by Sam Roberts indicates that

"According to Census Bureau estimates released last week, in the year ending July 1, 2013, the city recorded the third consecutive gain in its non-Hispanic white population.

During that same period, the city gained more people than it lost through migration. Neither of those gains has probably happened since the 1960s, according to demographers."

It is true that net migration, domestic and international, was positive between 2012 and 2013. However, net migration was also positive in the years ended 2012 and 2011, according to Census Bureau data. Among the three recent years, the lowest net migration total was in 2013 (Table).

| New York City Net Migration: 2011-2013 |

| Year |

Domestic |

International |

Combined |

| 2011 |

(55,807) |

69,076 |

13,269 |

| 2012 |

(64,383) |

71,752 |

7,369 |

| 2013 |

(67,629) |

73,615 |

5,986 |

| Total |

(187,819) |

214,443 |

26,624 |

| Data from Census Bureau |

|

Further, net domestic migration has continued to be negative. The city has lost a net 187,000 domestic migrants in the first three years of the decade. This is an average of more than 60,000 annually. This is, however, an improvement from the 2000s, when net domestic migration averaged a minus 135,000.

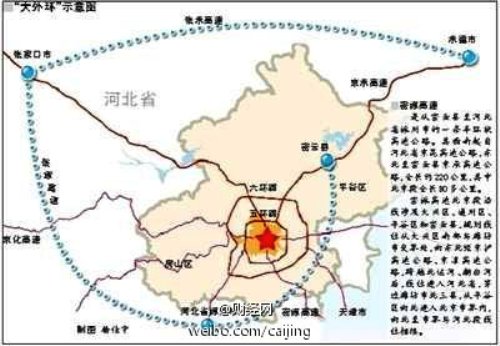

Today, there are about 30 megacities in the world, where more than 10 million residents live. The largest is Tokyo, at about 38 million. Recent announcements by the government of China could lead to the worlds' first gigacity (for want of a better term, used here to denote a city of more than 100,000,000 population, see note). According to the Nanfang Insider, the economic integration of megacity Beijing, megacity Tianjin and eight cities (prefectures) in the province of Hebei would result in a city of 130 million. China Daily is a bit more circumspect, indicating that the Beijing supercity would have only 85 million.

The giga/super city would be tied together by new rapid transit lines and highways and surrounded by the 7th Ring Road, adding to the six that have already been built. The 7th Ring Road would consist of two roads, circling most of the area, and extending to a combined 850 miles (2,200 kilometers). By comparison, London's M-25 is 117 miles long (188 kilometers), the Moscow MKAD 68 miles long (109 kilometers) and the Washington beltway is 64 miles long (103 kilometers)

The giga or super city is not likely to really be a city, because it would be much larger than a labor market (this is why the near continuous urbanization from Boston to Washington or Tokyo to Osaka-Kobe-Kyoto is not a city). The estimated land area is 67,000 square miles (175,000 square kilometers). This is nearly as large as Cambodia or the state of Oklahoma. Providing the point to point daily commuting in such a large area is well beyond the capability of any affordable transportation system. Star Trek like teleportation could do the trick. Meanwhile, however, there is plenty to be gained from the economic integration of this large area.

Graphic of the new 7th ring road from nanfang.com:

Note: Technically, a gigacity would need 1 billion people (10 to the 9th power). However, megacities, with their 10 million minimum are also wrongly named. A city with a mega city would have 1,000,000 people (10 to the 6th power). Artistic license justifies the gigacity term under the circumstances. Besides, with the slowing growth of world population, it seems unlikely than any city will achieve a population of 1 trillion.

|