The news that Goldman Sachs is facing civil fraud charges from the Securities and Exchange Commission came just days before a Washington Examiner story reported that Goldman Sachs, in the company’s annual letter to shareholders, reassured investors that the financial regulatory reform being voted on this week in Congress will “help Goldman’s bottom line.” Yikes!!

Since the autumn of 2008, all things concerning financial regulation have been moving very rapidly. I often find it impossible to stay in front of it. The legislation is barely made public before it is changed–they even change bills in the days after they are passed. This makes it really hard for the ordinary citizen or even an informed researcher to clearly see where there bill is finally.

Ultimately, this reminds me of a con game I’ve seen played on the streets in New York called Three-card Monte. It requires very fast hands to effectively manipulate the cards. As the professional con artist rapidly moves three cards – two aces and the queen of hearts – around the table, he challenges you to keep your eye on the queen. You are encouraged by the con and his shill – the co-conspirator among the audience – to place a bet on your ability to keep up with the movements. Of course, you can’t win because the game is fixed. But – and here’s why Goldman’s joy at the financial regulatory reform makes me nervous – you will think that you can win when you see the shill winning.

Everybody and their brother have gone on record with some argument for or against the current version of financial regulatory reform in Congress this week. The question most often asked is: Will it end “too big to fail?” In my view, it is not the size of the firms but the size of the risks that are the real problem. While I don’t mind losing $5 on a street corner, all Americans mind losing $3.8 trillion in the Bailout.

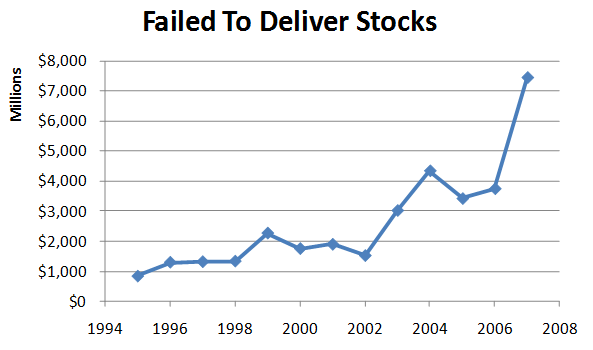

Here’s the heart of the problem. There is something going on back-stage at Wall Street called the centralized clearing and settlement system. I worked in it in the US and have studied and consulted to the system in the rest of the world. The system we have in the US was exported around the world thanks to the United States Agency for International Development. The system is designed to let all the stocks and bonds traded on the stock exchanges be paid for electronically. To expedite the process – known as settling trades in stocks, bonds and all the other financial instruments – the system accepts an electronic “IOU” for the shares until the real financial papers can be delivered. It requires that the money be paid immediately. The problem is that the system permits dealers to sell more stocks and bonds than exist without any incentive to deliver on time. The centralized settlement system simply holds the “failed to deliver” open indefinitely in the form of an electronic IOU. The value of the IOUs in the system has risen dramatically since 2001.

Source: Public data, available in annual reports of Depository Trust and Clearing Corporation and its subsidiaries.

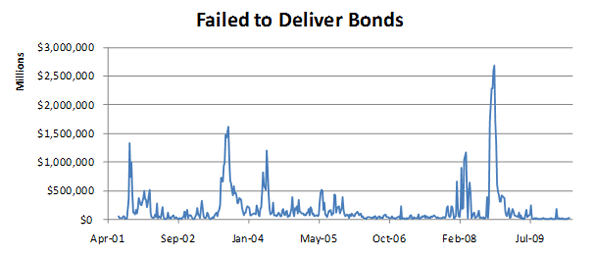

Source: Public data, available from the Federal Reserve Bank of New York.

Notice the relationship of the timing of the spike in the bond failures to the financial crisis: the 17 primary dealers reporting to the New York Federal Reserve Bank failed to deliver about $2.5 trillion worth of US Treasury securities for 7 weeks in late 2008 – no fines, no sanctions; worst of all, very little press coverage.

This is the core of the problem – both in practice and in theory. This means supply is infinite – there is no limit to how many bonds can be sold because no one is enforcing delivery. In reality, no one should be able to sell more US Government bonds than the US Government has issued. That’s a problem in the practices supported by the system. The theoretical problem is that all financial instruments, including the bonds issued by city and state governments,, are being sold without any attachment to the real assets. This damages not only buyers in the stock market, but also the companies and governments who are trying to raise the money needed to keep delivering the services that we depend on them to provide.

The practice of allowing the delivery of electronic IOUs in place of shares of stock or Treasury bills is a process that rewards financial manipulation instead of allocating resources to productive uses – the activity that capital markets should be doing. All the Congressional and the Administration talk about Wall Street reform is to centralize more trades into the existing settlement system – the one with the trillion-dollar hole in it! Someone has convinced them that the centralized system can easily track and account for positions – the actual statistics present a very different picture.

Stop content thief

Plagiarism Avenger can prevent content thief. STOP Content Thieves from Ranking Above You! Plagiarism Avenger Review

It's Getting Worse, Not Better

Fails to deliver in Mortgage Backed Securities passed the trillion dollar mark for the week ending May 19, 2010: $1,057,586,000,000 bonds went undelivered for settlement just by the 17 Primary Dealers.

I read both the House and Senate versions of the Financial Regulatory Reform bills they passed: nothing in there fixes this problem of fails to deliver for any securities. Print this story and fax it to your Senators and Representatives. If they don't do something now, there is nothing to prevent September 2008 from happening again this month.

If you can stand the technical details, you can download my bond research from 2007 which describes how this happens, how long it's been going on and what it means for investors.

Thanks for reading!

Follow me on Twitter: SusanneTrimbath